CVAE: details on the calculation of the added value

The tax authorities have just integrated into their documentation the clarifications resulting from various judgments and judgments relating to the determination of the added value taxable at the CVAE (BOFiP news of September 7, 2016).

Principle of calculation of added value ¶

Companies whose turnover exceeds €500,000 are subject to the contribution on the added value of companies (CVAE). This tax is determined by multiplying the added value produced by the company at a rate whose level depends on turnover. This added value (VA) is not calculated in the same way as the VA within the meaning of intermediate management balances (SIG), or as the VA used to calculate the special profit-sharing reserve (RSP) for the profit-sharing of employees on benefits.

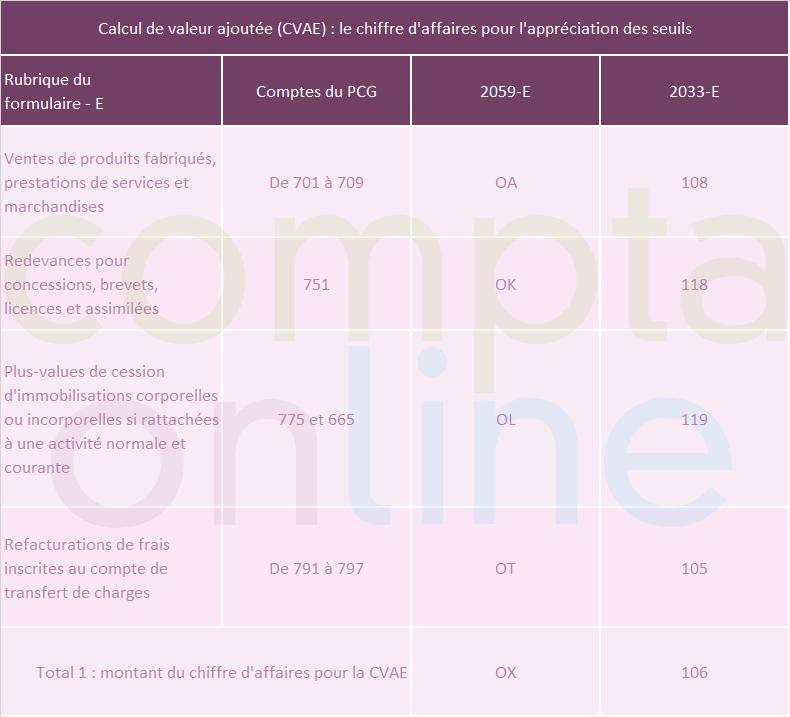

For the CVAE tax base, the added value is obtained by the difference between certain income and certain expenses.

|

Products used for the calculation of the tax VA | Expenses retained for the calculation of the tax VA |

¶

Taxes and duties deductible from the added value ¶

Taxes and duties (accounts 63) are not deductible from the added value subject to CVAE at the exception of those which directly affect the price of the goods and services sold by the person liable.

During several cases, the Council of State had to rule on the taxes accepted or not as a deduction from the VA. The tax authorities have just integrated these case law into their documentation.

| Taxes and duties deductible from VA | Taxes and duties not deductible from VA |

Excerpt from BOFiP news of September 7, 2016

By chatlivecamsex